Renovating the kitchen, tricking out the bathroom or creating a relationship-saving man cave or she shed is now more doable than at any time since the financial crisis. Rising home values have pushed up our collective home equity, which is the value of our lairs minus the mortgage balance.

And we’re increasingly eager to scratch our upgrade itch. Homeowners are expected to shell out more than $350 billion for remodeling projects in the 12 months through September 2019, a 30% rise in just three years.

There are two ways to tap home equity. A classic home equity loan (HEL) is a standard fixed- loan. You get a chunk of money upfront, and then pay it back over a set period of time of five to 10 years, or longer.

Home Equity Loans Make A Cautious Return

For years, home equity lines of credit (HELOCs) have been far more popular than HELs. A HELOC works a lot like a credit card: You have a credit limit you can borrow against (typically for 10 years), and any time you pay back any money, you regain borrowing capacity. The interest on HELOCs is variable, not fixed.

HELOCs have become even more popular since the financial crisis, as a change in lender regulations makes it more expensive for lenders to offer HELs.

It’s important to understand that the Federal Reserve is pulling the strings behind the curtain of HELOC s. The Fed determines the trajectory of short-term interest s through its Federal Funds . And most HELOC interest s are based on a formula that starts with the Fed Funds (or other short-term indexes) and then adds a few percentage points of “margin.”

Germany Long Term Interest Rate, 1993

From 2008 through most of 2015, the Federal Reserve kept the Federal Funds near zero, as a way to encourage more economic growth coming out of the financial crisis. That made HELOCs a screaming deal, with s as low as 3% or so.

But with signs that the economy is in fact doing much better, the Fed has been slowly raising its target interest from the abnormal zero level. The Fed Funds is now above 2%. -watching experts give a high probability that by the fall of 2019, the Fed Funds will be in the vicinity of 2.5%.

That means that if you use a HELOC with a variable interest , you may likely be setting yourself up for higher s, and higher payments, in the future.

Surprising Home Equity Statistics

For a big renovation project that you expect to need three, five or even 10 years to pay back, locking in the fixed of a classic HEL could be a financially smart move for the longer-term; it’ll also give you peace of mind that you won’t have any payment shocks in the future. Many credit unions continue to offer home equity loans.

A $50, 000 draw on a HELOC that you take 10 years to pay back will run you about $555 a month at today’s 6% average . If the rises to 7%, you’re looking at a payment of $580. If s creep higher, so too will your HELOC tab. (You can run the numbers using different assumptions.) Opt for a HEL and at today’s average 6.4% interest you can lock in a monthly payment of around $565, which won’t budge over the life of a 10-year payback.

Another option is to consider a newer twist in home equity borrowing: a hybrid HELOC that gives you the option of converting from the variable to a fixed . Just be sure you understand when you can convert and what your fixed will be. The fixed will obviously be higher than the variable. The peace of mind may be worth it, especially if you expect to take many years – not months – to repay the line.

How To Increase Your Home Equity Loan Volume After The Pandemic

All information provided in this publication is for informational and educational purposes only, and in no way is any of the content contained herein to be construed as financial, investment, or legal advice or instruction. Guaranteed , Inc. does not guarantee the quality, accuracy, completeness or timelines of the information in this publication. While efforts are made to verify the information provided, the information should not be assumed to be error free. Some information in the publication may have been provided by third parties and has not necessarily been verified by Guaranteed , Inc. Guaranteed , Inc. its affiliates and subsidiaries do not assume any liability for the information contained herein, be it direct, indirect, consequential, special, or exemplary, or other damages whatsoever and howsoever caused, arising out of or in connection with the use of this publication or in reliance on the information, including any personal or pecuniary loss, whether the action is in contract, tort (including negligence) or other tortious action.

Housing market information is provided by Altos Research, Inc. based on analysis of all active market properties for sale in the US in the preceding week. All analytics are copyright Altos Research and not affiliated with any MLS.As the Federal Reserve increases interest rates in an attempt to lower inflation, a confluence of factors point toward home equity growth opportunities for financial institutions. With dramatic changes in the mortgage market, soaring home values and a shift in market share among institutions competing in this space, what can your organization do to win its fair share of the market opportunity?

Rising interest rates mark the unofficial end to the refinance boom initiated at the start of the COVID-19 pandemic. With 30-year fixed mortgage rates having hovered in the 3% range for much of 2020 and 2021, homeowners refinanced their existing mortgages at unprecedented rates. Refinanced mortgages accounted for 64% and 59% of one- to four-family mortgage originations in 2020 and 2021, respectively. Based on projections from the Mortgage Bankers Association, and with rates increasing, this refinance share is expected to level off at 33% in 2022 and 26% in 2023. In short, the majority of qualified homeowners for whom it would be advantageous to refinance have likely already done so in the last two years.

Home Equity Loan And Heloc Guide

Another byproduct of the two-year refinance mania is its impact on outstanding home equity balances. At the end of 2019, the Federal Reserve reported $501 billion in outstanding home equity balances. This total had dropped to $396 billion by the fourth quarter of 2021. At least part of this 21% decline can be attributed to consumers consolidating debt and rolling their equity balances into their refinanced first mortgage.

Although the decline in home equity balances accelerated during the pandemic-initiated low-rate environment, it is not a new trend. In fact, ever since the sharp and unsustainable increases in home equity balances in the years leading up to the financial and housing crisis in 2008, home equity balances have steadily declined. While Great Recession–era charge-offs, declining home values and overleveraged homeowners contributed to the initial drop in home equity balances, the ongoing decline suggests there may be more at play in both lenders’ and borrowers’ relationships with home equity loans.

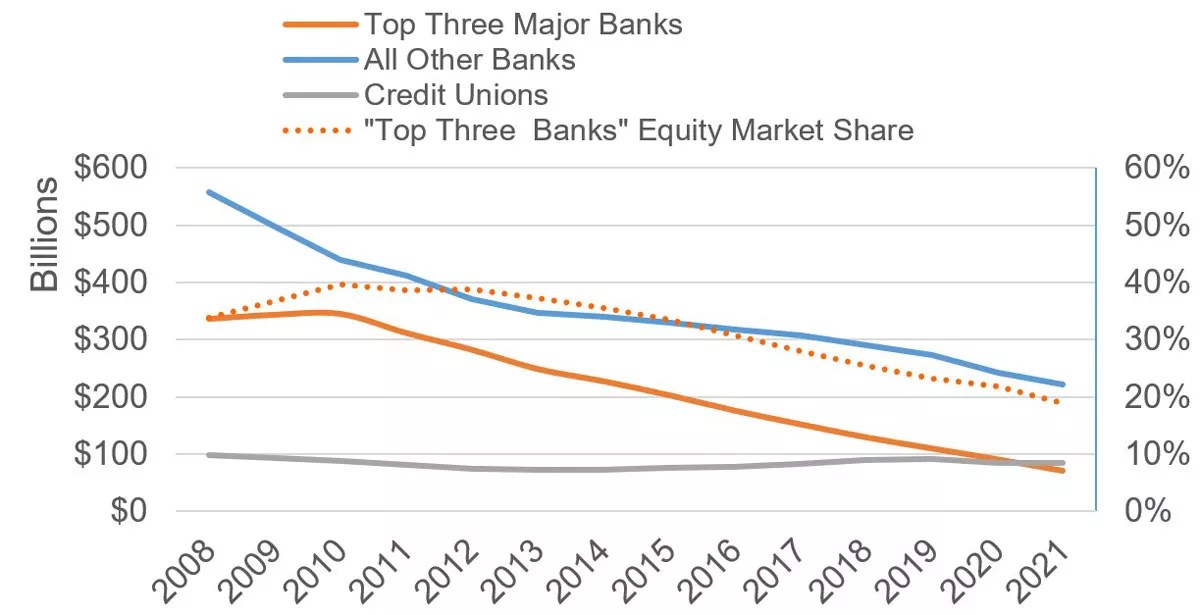

Part of the steady decline since the Great Recession includes a significant shift in the home equity market share controlled by the three largest retail banks. Bank of America, Wells Fargo, and Chase collectively accounted for 40% of all outstanding home equity loan balances in 2010. The same equity market share is only 19% today.

Helocs Set To Rise In 2018

Whatever the reasons for this strategic shift in the loan portfolio mix, it represents an opportunity for other financial institutions to fill the gap. While other banks in totality follow a similar trend line as their big bank brethren, credit unions as a group experienced a 28% increase in overall home equity balances between 2013 and 2019, offsetting the 26% decline seen during the five years prior to 2013. Credit unions have not been immune to the decline in balances during the pandemic though. Despite strong balance growth and increased market share over the last decade, data from credit unions participating in ’s Performance Analytics benchmarking program shows that equity lending has played a diminishing role in loan operations. This is evidenced by the 5.2% of credit union member households that had an equity loan in 2006 (pre–Great Recession) dropping to 4.8% in 2011 (post–Great Recession), 4.1% in 2016 (prepandemic) and 3.6% in 2021 (postpandemic onset). In other words, credit unions may have experienced balance growth, but it did not exceed the pace of household growth.

A combination of low rates and an imbalance in housing supply and demand driven by demography changes in the U.S. has created a red-hot real estate market in many areas of the country. Home values have soared as demand exceeds supply and homebuyers capitalize on the low-rate environment to stretch their mortgage dollars further. The $295k median home price for existing homes in 2020 rose to $344k in 2021 and is expected to reach $373k in 2022 according to projections from the Mortgage Bankers Association. Median prices for new homes follow a similar trend, going from $335k in 2020 to $427k in 2022. As we know, all good things (at least for sellers) must

0 comments:

Post a Comment